January 21, 2026

Understanding The Rising Cost Of Renters Insurance

Renters and their personal property can be just as vulnerable to theft, damage, and visitor injury as homeowners.

If you lease a space, you’ve got fewer home-maintenance things to worry about than homeowners do. But renters and their personal property can be just as vulnerable to theft, damage, and visitor injury. That’s why it’s smart to purchase renters insurance.

The problem is, these days renters’ insurance premiums are on the rise. The Zebra explores the reasons why, areas where renters insurance is the least affordable, additional coverage to consider, and helpful strategies to keep those premiums affordable.

Why Renters Insurance Costs Are Rising

The average cost of renters insurance nationally is around $171 annually, based on the latest data from the Insurance Information Institute. While that’s a slight increase from the previous year, renters’ insurance rates have actually come down 9% since 2013.

According to Gitnux, the average monthly premium is $15, with Mississippi being the state with the highest average renters insurance rates at approximately $252 per year.

A 2024 report by the Federal Reserve Bank of Philadelphia found that more rental insurance policyholders (by 23.5 percentage points) experienced year-over-year premium increases than those who reported premium decreases.

Among the culprits? Inflation, increased crime rates, higher coverage limits, and severe weather claims (more on this next). Consider that the average property damage loss per renters insurance claim is estimated at $10,000. Lightning and fire claims are the most costly associated loss, averaging more than $11,000 per claim, while theft comprises almost 1 in 5 renters insurance claims, per Gitnux.

“Higher local crime rates, liability claims, and medical expenses all contribute to higher rates, as does inflation and personal property values. The cost of household goods, ranging from electronics to furniture, has increased, leading insurers to adjust the contents coverage and raise overall premiums,” says Maya-Rae Woods, an account manager with All Solutions Insurance Agency LLC.

Dennis Shirshikov, a professor of finance and economics at City University of New York/Queens College, also points to higher construction labor costs, steeper replacement material prices, increases in theft claims in dense urban areas, and elevated liability payouts.

“Insurers have also adjusted premiums to reflect reinsurance costs that climbed during recent years of heightened catastrophic events, and this cost is passed through to policyholders,” he adds.

Truth is, renters insurance prices are going up for many of the same reasons why everything else in the economy feels more expensive, according to Beth Swanson, an insurance analyst for TheZebra.com.

“The encouraging news is that premium increases have generally been smaller than what we are seeing in homeowners or auto insurance premiums, largely because renters policies start from a lower baseline cost,” she says.

Yet only 55% of renters currently have a renters insurance policy—61 million people—versus 95% of homeowners, The Zebra reports.

How Climate Risks Are Reshaping Renters Insurance

Among those who filed renters insurance claims in 2024, 66.8% attributed those claims to a natural disaster or weather event, per the Federal Reserve Bank of Philadelphia.

“The increasing frequency and severity of hurricanes, floods, wildfires, and intense storms elevate the payout of expected claims and increase exposure,” explains Rami Sneineh, vice president at Insurance Navy Brokers. “As a result, many insurers have tightened underwriting, increased premiums in exposed ZIP codes, narrowed coverages, or requested increased rates among insurance regulators.”

Amplified climate risks have made it unprofitable for carriers to operate in some areas.

“This results in one or two insurers with a monopoly over an entire county at times, leaving renters to pay higher premiums,” continues Woods.

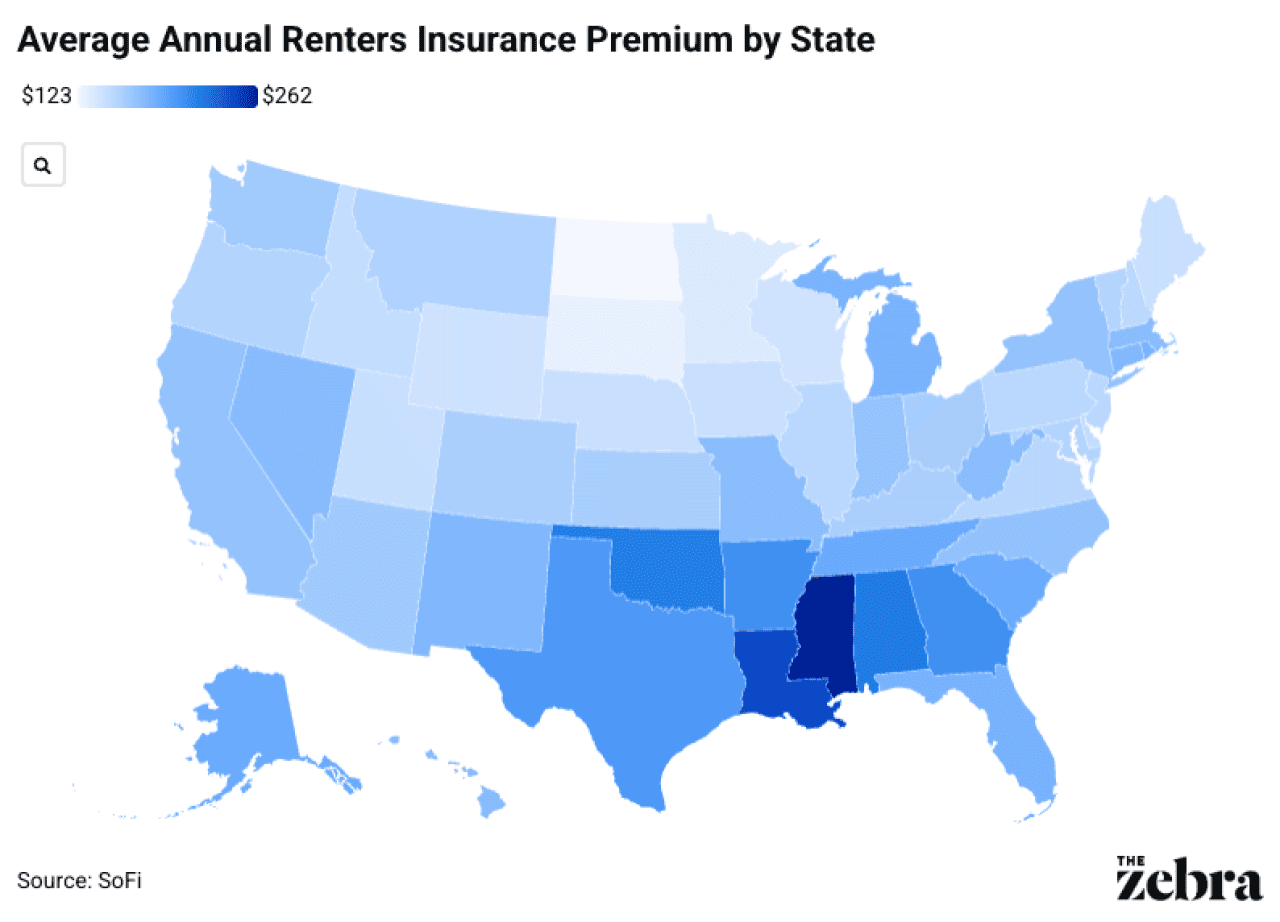

Where Renters Insurance Is Most Expensive

Curious where renters’ insurance costs the most? Here’s a quick breakdown based on the latest findings from SoFi:

- Mississippi: $262 per year

- Louisiana: $243

- Alabama: $219

- Oklahoma: $216

- Arkansas: $205 (tied)

- Georgia: $205 (tied)

- Texas: $199

- Tennessee: $187

- Alaska: $186 (tied)

- South Carolina: $186 (tied)

“Insurance for renters is very similar to real estate – what you pay will depend on location,” says Michael Silverman, president/CEO of Silver Lining Insurance Agency. “Cities are traditionally more expensive for insurance due to claims exposure and the fact that there are more people and thus higher crime rates. Coastal locations are higher in premiums or, at times, not available due to the potential for claims caused by various storms.”

The South suffers from some of the most expensive rates in the nation, especially in states like Mississippi, Louisiana, and Georgia.

“And in Detroit, renters are unfortunately paying three times more, or 260% higher than the national average,” Woods notes. “Not only does Detroit deal with multiple climate hazards, but also a significant number of fire incidents and elevated crime rates.”

ZIP code level variation can be substantial because insurers price based on historical loss data, population density, crime patterns, and even proximity to fire response services, which can differ within the same city by only a few blocks.

Cities Where Renters Insurance Is Still Affordable

Realtor Ryan Fitzgerald, founder of Raleigh Realty, says lower-risk inland metros continue to price renters’ insurance more affordably, particularly where severe weather and property crime are modest.

“Cities like Omaha, Des Moines, Madison, Columbus, Boise, and Spokane benefit from strong fire protection, newer housing stock, and fewer large losses,” he says. “Meanwhile, in the southeast, inland suburban ZIP codes away from the coast frequently quote better than dense cores, and high-growth suburban communities with modern, sprinklered buildings can rate favorably as well.”

Woods notes that California cities like Chula Vista, San Diego, San Jose, and Irvine comprise some of the lowest premium averages in the state at around $16 per month, although California residents in general pay about $38 more than most states in the country.

“Nationwide, Delaware is shown to be the least expensive state for renters insurance, and Rapid City in South Dakota is the least expensive city,” adds Woods.

Renters’ Rights That Affect Insurance Costs

Although renters’ insurance is not legally mandated in any state, your landlord may require that you carry the standard personal property coverage and the addition of liability coverage in order to sign a lease. In fact, three out of four landlords currently require tenants to show proof of renters’ insurance before signing a lease, per Gitnux.

“Renters are responsible for everything within the walls of their unit, while the building owner, landlord, or property management company is responsible for the structure, including all common areas,” says Mark Friedlander, senior director of Media Relations for the Insurance Information Institute.

Be aware that landlords cannot require you to have add-on protections like flood or earthquake insurance.

“If you believe you are facing unfair rental insurance pricing, you can file a complaint with your state’s department of insurance, which regulates rate filings and investigates potential pricing violations,” suggests Shirshikov.

When Renters Need Additional Coverage

A standard renters insurance policy, sometimes referred to as tenant’s insurance, includes three basic types of protection.

Personal possessions coverage

This protects your personal belongings (furniture, clothing, electronics, appliances, artwork, and jewelry) against damage from fire, smoke, lightning, vandalism, theft, explosion, windstorm, water, and other hazards listed in the policy.

Liability coverage

This safeguards against lawsuits for bodily injury or property damage that you or your family members cause to other people, and also pays for damage your pets cause. Additionally, it covers the cost of defending you in court, up to the limit of the policy. “A standard policy also provides no-fault medical coverage. So, if a friend or neighbor is injured in your home, you can submit their medical bills directly to your insurance company,” Friedlander adds.

Additional living expenses coverage

If your rental is destroyed by a disaster that your policy covers and you need to live somewhere else, this covers your additional living expenses (hotel bills, temporary rentals, and restaurant meals) up to the terms of the policy.

Be aware that minimum coverage limits often fall short due to rising liability exposure and because the cost of replacing even a modest amount of personal property has increased faster than the traditional policy benchmarks. That’s why it’s smart to consider paying for higher levels of coverage, including replacement cost coverage (which reimburses based on the current replacement value for your possessions) over actual cash value coverage, which factors depreciation into your claim payout for a covered loss.

“The easiest way to determine what kind of and how much renters insurance coverage you should purchase is to create a home inventory—a detailed list of all your personal possessions, with their estimated value,” recommends Friedlander. “There are also numerous endorsements or separate policies you can purchase to enhance your coverage. This includes excluded perils such as floods and earthquakes. You can also buy an endorsement to enhance coverage for high-value items such as fine jewelry and fine art.”

Swanson additionally recommends considering water backup coverage, “since damage from back-up drains or sump pumps isn’t included in most standard policies. Some insurers also offer identity theft protection and expanded pet liability coverage, which can be helpful, depending on your lifestyle.”

How Renters Can Reduce Their Premiums

Eager to lower your out-of-pocket costs for renters coverage? Follow these best practices, as suggested by the experts:

- Shop around among several different carriers

“Get price quotes from many different insurers and independent agents to find the best deal,” says Sneineh. - Choose a higher deductible

The higher your deductible, the lower your premiums, and vice versa. - Bundle coverages

“Bundle your rental coverage with an auto insurance policy or another policy offered by your insurer, such as life insurance or pet insurance,” advises Friedlander. - Add safety features

Install safety features like smoke detectors and monitored alarm systems. - Inquire about discounts

Look for discounts you may be eligible for, including having a claims-free history, being a loyal customer, enrolling in paperless billing and autopay, and paying your premium annually. - Carefully document your belongings

“This reduces the likelihood of disputes during a claim and helps you avoid small claims that may lead to surcharges,” explains Shirshikov. - Maintain a strong credit profile

“Insurers use credit-based insurance scores that influence pricing in many states,” Shirshikov says.

Key Takeaways for Renters in High-Cost Cities

Fact is, even if you live in a market where premiums are higher than average, renters insurance remains one of the most affordable forms of coverage you can get for your personal belongings and peace of mind. Take the time to better understand the factors behind rate increases, including your location and creditworthiness, and how you can pay less for a policy.

“Also, carefully review your policy annually to adjust coverage for life changes, new purchases, or shifts in local risk conditions,” recommends Shirshikov. “The most cost-effective strategy is to be proactive rather than reactive as a renter with coverage.”

This story was produced by TheZebra and reviewed and distributed by Stacker.

RELATED CONTENT: Plain and Simple: The 4 Most Overlooked Insurance Policies You Should Carry