New Hampshire Teacher Fired After Allegedly Driving Student To Get Abortion

The teacher reportedly had been conversing with the student for over 2 weeks about the medical appointment.

A New Hampshire educator was terminated after reportedly assisting a student in obtaining an abortion without parental knowledge.

A New Hampshire Department of Education report indicates that the teacher had been advising the student about a medical appointment for weeks. On the day of the procedure, the educator called in sick, citing food poisoning, to transport the student to a clinic during school hours. The report confirmed that the educator’s claim of food poisoning was false. However, the teacher said the student had no support from anyone, “so they offered to go with them.”

State Rep. Erica Layon expressed her dismay, stating, “I am horrified to hear that a teacher in our New Hampshire schools felt the right way to help a pregnant student who felt unsupported in her pregnancy was to research abortion facilities and call out sick to take a student to an abortion rather than to help her speak with her parents and find support from her family.”

State Sen. Tim Lang emphasized the importance of transparency in schools, asserting, “Parents have the right to know everything that is happening to their child in school. Keeping secrets or going behind a parent’s back is never good public policy.” He further explained that such behavior sets a troubling precedent for youth, and when authority figures engage in deceitful behavior, it implicitly condones dishonesty, which can negatively shape future generations.

Melanie Israel from The Heritage Foundation noted that students typically require parental consent for off-campus activities. Planned Parenthood confirms that New Hampshire law mandates that for individuals under 18 seeking an abortion, a parent must be notified 48 hours before the procedure.

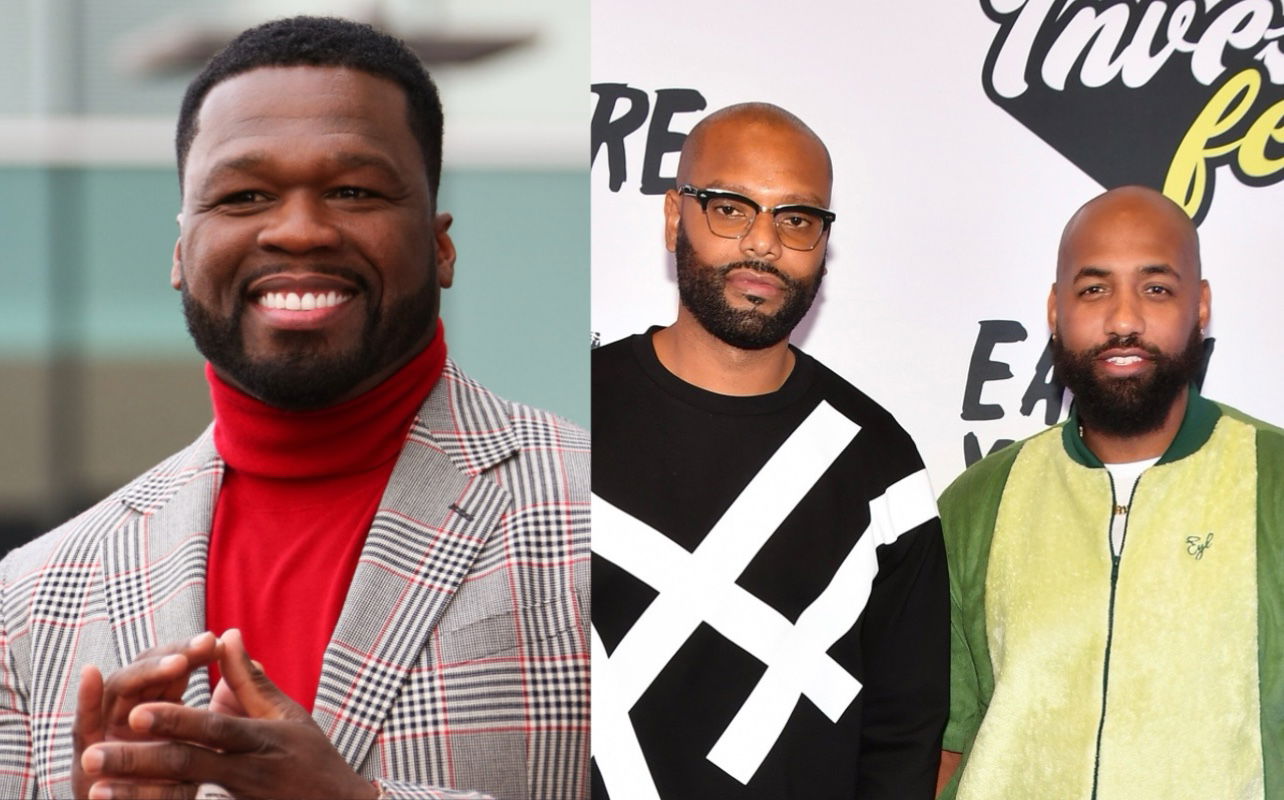

And in a June 26 social media post, they confirmed that 50 Cent will headline the fourth annual event, which will be co-sponsored by sponsored by Steve Harvey, Matthew Garland, and Michael MacDonald.

“We believe [50’s] insights and experiences will inspire and empower our audience to pursue their own paths to financial freedom,” Bilal added.

The conference, which has been in Atlanta every year, is designed after the podcast Earn Your Leisure, which aims to empower the Black community when it comes to financial decisions. The conference last year brought approximately 50,000 attendees to the Georgia World Congress Center over three days.

Organizers anticipate this year’s conference will draw around 60,000 participants.

“Being around thousands of people is more productive for you on an inspirational, motivational standpoint,” said about the conference in March, according to The Atlanta Journal-Constitution.

According to Bilal, the $250 price for the three-day conference will be beneficial to those who attend.

“There’s a reason why people go to church, there’s a reason why people go on pilgrimages, right?” he said. “Being around thousands of people is more productive for you as far as on an inspirational, motivational standpoint than just being in your room by yourself.”

Black Alabama Mayor Will Finally Take Office After Settling Lawsuit Against Obstinate Town Council

'I’m pleased with the outcome and the community is pleased. I think they are more pleased that they can voice their opinion and vote.'

Last summer, a Black man who was rightfully elected mayor in a small town in Alabama sued the town’s council members, accusing them of conspiring to hold an illegal election to reappoint the previous mayor and keep him out of office.

After a proposed agreement between the town and the soon-to-be mayor, he will become the first Black mayor to hold the position in the small town.

According to The Associated Press, Patrick Braxton should be recognized as mayor of Newbern if a judge approves the terms of an agreement between Braxton and the town of Newbern. Paperwork filed on June 21 should allow the town’s first Black mayor to take the position and permit the seating of a new city council if U.S. District Judge Kristi K. DuBose gives the green light to the proposal.

“I’m pleased with the outcome, and the community is pleased. I think they are more pleased that they can voice their opinion and vote,” Braxton, 57, said.

Newbern, which has 133 residents, has a mayor-council government, but the town has not held elections for the past 60 years. Traditionally, the mayor would appoint his successor, while the successor appointed the council members. In a town that is overwhelmingly Black by a 2-1 margin, the mayor and council members were always white, according to the lawsuit filed by Braxton and others.

In 2020, Braxton decided to run for mayor of Newbern. Being the only person on the ballot, he was voted in and became the town’s mayor-elect. After winning the election, he appointed council members but was met with resistance from the previous mayor and council members.

In the lawsuit against Newbern, Braxton alleged that town officials “conspired to prevent the first Black mayor from exercising the duties and powers of his new job” and also prevented the town’s first majority-Black council from being seated.,The town officials changed the locks and refused to give Braxton access to town bank accounts. They also allegedly conspired to set up a special election and “fraudulently reappointed themselves as the town council.”

Under the proposed settlement, Braxton will take office as Newbern’s mayor and be granted town hall access. All “individuals holding themselves out as town officials will effectively resign and cease all responsibilities with respect to serving in any town position or maintaining any town property or accounts,” the agreement states.

Positions will be filled by appointment or through a special election. The town will hold municipal elections in 2025.

Trump and Former White House Administrators Attack Biden’s Mental Capacity By Calling For A Drug Test Before Debate

This is getting weird....

Former President Donald Trump thinks the only reason President Joe Biden performs well in debates is by using performance-enhancement drugs — so he wants the President to take a drug test.

Trump made the claims on his Truth Social site on June 24, just three days before the two battle it out for the first round of debates on June 27 in Atlanta. “Drug test for crooked Joe Biden??” Trump wrote in all caps.

His idea came about after former White House physician Rep. Ronny Jackson (R-Tx.) said during an interview with Fox News that Biden should submit to a drug test — before and after the debate.

“It’s really embarrassing as the former White House physician to have to do something like this, but we don’t have any choice based on what’s going on,” he said. “But I’m going to be demanding on behalf of many millions of concerned Americans right now that he submit to a drug test before and after this debate, specifically looking for performance-enhancement drugs.”

Jackson continued to suggest that Biden was “different” during the State of the Union Address (SOTU) in March 2024 and thinks he was “on something.”

The Republican congressman even speculated that Biden is having drugs given to him while he visits Camp David — the presidential retreat — in late June as he prepares for the debate. “I feel like this is probably what’s going on over this week at Camp David,” Jackson said.

“Part of that is probably experimenting with just getting the doses just right because they have to treat his cognition.”

The narrative has been pushed by Trump and his band of allies for months. On June 15, Trump went before a crowd in Detroit, suggesting that Biden didn’t know what the word “inflation” meant. He challenged Biden to take a cognitive test — one he was said to have “aced.” According to Forbes, Rep. Mariannette Miller-Meeks (R-Iowa) shared similar sentiments with Jackson during a Fox Business interview. She spoke on behalf of all GOP legislators, saying the party expects the president “will be on something” during the debate.

After the Biden administration caught wind of Jackson’s comments, the team brushed it off, and White House spokesperson Andrew Bates said Republicans are intimidated by the country’s leader. “It’s telling that Republican officials are unable to stop announcing how intimidated they remain by the President’s State of the Union performance,” Bates said.

During Biden’s annual physical in February, medical professionals revealed the President is “fit for duty” with no signs of concern. He also went through a neurologic exam, and while there were no signs of “any cerebellar or other central neurological disorder,” the President does suffer from peripheral neuropathy, which is nerve damage causing pain and sometimes numbness in his feet.

Legislators announced the impressive new budget on June 22 with some of the specifics that go along with it. Allotted money will support several proposals–15 in total–drafted by the Legislative Black Caucus, such as having the Golden State issue an apology for the pain and suffering inflicted on Black Californians during slavery.

Assemblywoman Lori Wilson called the move “a win” because, in addition to the bills, the budget will support two constitutional amendments, including one that has yet to be drafted. “Even in a challenging deficit year, we’ve had our leadership and the governor recognize the obligation to those impacted by slavery,” Wilson said.

The approval was exactly what Black lawmakers hoped for after a yearlong battle following task force study results examining how lawmakers could enact reparations. However, not all residents are on board with the idea. In September 2023, a poll from the University of California, Berkeley revealed several residents were against Black residents receiving any form of reparations, including cash payments.

Fifty-nine percent of participants rejected the cash payments idea, 76% of Black respondents were in favor, and 66% of white voters opposed the idea.

While many Californians appear to be looking forward to the measure, which is the first of its kind at the state level, lawmakers are scheduled to take a statewide tour to discuss the study, the next steps, and what residents think.

California Democrats started the conversation, and other state leaders are considering similar moves. In December 2023, New York Gov. Kathy Hochul signed a bill that would create a reparations commission to study the state’s history of slavery and racism.

Some of the other proposed bills align with creating the California American Freedmen Affairs Agency, created by Sen. Steven Bradford. The new department will prevent the state from punishing prison inmates who refuse to work and curate a grant program that funds community efforts to limit crime in neighborhoods and schools. Under Bradford’s leadership, the agency will also investigate racially motivated eminent domain cases, which grants the government the power to take private property and convert it into public.

According to the Los Angeles Times, Bradford has been working with descendants of California residents who have lost out on financial gains from properties they were forced to sell. “There are multiple examples of African American families who were forced off their land for no other reason than they didn’t want them there anymore,” Bradford said.

“And now their homes have been replaced with freeways or parking lots, or as in Manhattan Beach, an alleged park that was 40 years before it even came into development.”

Bradford’s reparations legislation would also determine how valid claims are brought up by families who feel their property was unjustly seized. The Office of Legal Affairs would take on cases to present potential remedies for offenders of eminent domain, such as having the property returned or monetary payments.

All bills are expected to pass by the end of the legislative session on Aug. 31.

Cozy Up By The Pool With Books By Black Female Authors

Originally Published Jun. 30, 2021.

Summer is here. Just because school is out doesn’t mean we should stop exercising our brains. Reading is a great activity, whether you choose to escape the sweltering sun and vacation in the mountains or you embrace the heat and go to the beach. The following is a list of 10 must-read books by black female authors that should be on your summer reading list.

We Should All Be Millionaires (Rachel Rodgers)

We Should all be Millionaires, a Wall Street Journal best-seller, aims to change the way women think about money and their ability to earn it. Rachel Rodgers is a CEO, business coach, mother, wife and intellectual property lawyer who founded Hello Seven to help women scale their businesses and get their earnings to seven-figures without sacrificing their families or their sanity.

With a 4.6/5 rating on Good Reads, a 5/5 on Barnes & Noble, a 5-star rating on Amazon and a 4.9/5 on Audible, it’s safe to say we aren’t the only ones digging this one!

Professional Troublemaker (Luvvie Ajayi Jones)

If overcoming your fears to achieve your goals is the mission, let’s call Luvvie Ajayi Jones the mission controller. But, you know, a cool one — the type who makes you laugh, while barking orders and reading you for filth. Prepare to be motivated into action and laugh until your sides hurt.

Ajayi Jones is a 2x New York Times best-selling author, a podcast host, keynote speaker (who slayed the TED stage), certified sneaker-head, and a hilariously witty “Professional Troublemaker” who doesn’t hold her tongue. Read her book Professional Troublemaker: The Fear-Fighter Manual then go grab her first one, I’m Judging You: The Do Better Manual. You can thank us later.

Wings of Ebony (J. Elle)

If you want to escape reality for a bit (we don’t blame you!), this instant New York Times best-selling fantasy novel may be the one for you. In this entrancing, powerfully moving debut, a Black teen from Houston has her world turned upside down when she learns about her godly ancestry and has to save both the god and human worlds.

In Wings of Ebony, Rue, the protagonist, is the only half-god, half-human in her world. A world where the “leaders protect their magical powers at all costs and thrive on human suffering.”

To celebrate the 20th anniversary of her best-selling book, Sacred Woman, Queen Afua released a special edition featuring two exciting new chapters. Queen Afua is a highly sought-after master herbalist, often called on by the likes of Jada Pinkett-Smith, Erykah Badu, and Mya, to understand how to harness the power of food. With over 50 years of experience helping others on their journey to green living and detoxing properly, this book truly encompasses her life’s work.

“Queen Afua teaches us how to love and rejoice in our bodies by spiritualizing the words we speak, the foods we eat, the relationships we attract, the spaces we live and work in, and the transcendent woman spirit we manifest.”

Bamboozled by Jesus (Yvonne Orji)

Actress and stand-up comedian, Yvonne Orji, known best for her role as Molly on Issa Rae’s hit series Insecureis delivering a hilarious mix of comedy, bible study, and memoir in Bamboozled by Jesus. Orji believes God is a prankster, and shares how he tricked her into living her wildest dreams.

The publisher describes it best: “This ain’t your mama’s Bible study. Yvonne infuses wit and heart in sharing pointers like why the way up is sometimes down, and how fear is synonymous to food poisoning. Her joyful, confident approach to God will inspire everyone to catapult themselves out of the mundane and into the magnificent.”

Get Over ‘I Got It’ (Elayne Fluker)

In this book, the author teaches us how to “Stop playing superwoman, get support, and remember that having it all doesn’t mean doing it all alone,” which is actually the subtitle. If you’ve suffered from feeling the need to do it all, this is the one for you as Fluker, who knows a thing (or five!) about having a busy plate, takes you by the hand, teaching you how to ask for the support you need.

During the author’s 20-year media career, she’s held top editorial positions at Martha Stewart Living, iVillage.com, Condé Nast Digital, Essence, Latina and Vibe. As a women’s advocate, podcast host, journalist, and media expert, Elayne Fluker has appeared in front of millions and is now here to tell millions why getting support is sexy.

What Would Frida Do (Arianna Davis)

Arianna Davis, Oprah Daily’s Senior Director in charge of editorial and strategy, decided to write a unique, motivating biography on Frida. Frida Kahlo, born Magdalena Carmen Frida Kahlo y Calderón, was a Mexican artist best known for her beautiful self-portraits, catchy quotes, and unibrow. She was also a feminist. A force. A woman ahead of her time who endured a lot more than met the eye.

In this book, the author helps you to find some of you in the way Frida lived. What Would Frida Do is educational, ridiculously self-reflective and inspiring.

Get Good with Money (Tiffany Aliche)

We can all benefit from getting better at managing our finances and in this New York Times, Wall Street Journal and USA Today best-selling book, the Budgetnista shares 10 steps to make readers financially whole.

“Tiffany Aliche was a successful pre-school teacher with a healthy nest egg when a recession and advice from a shady advisor put her out of a job and into a huge financial hole. As she began to chart the path to her own financial rescue, the outline of her ten-step formula for attaining both financial security and peace of mind began to take shape. These principles have now helped more than one million women worldwide save and pay off millions in debt, and begin planning for a richer life.” In other words, if you want to sort your financial life out, grab Get Good With Money.

Yoke (Jessamyn Stanley)

Jessamyn Stanley, a body positivity advocate, yoga teacher, and author, shares a collection of extremely candid, humorous autobiographical essays, diving into the topics of self-love, imposter syndrome, cannabis and more.

“In Sanskrit, yoga means to “yoke.” To yoke mind and body, movement and breath, light and dark, the good and the bad. This larger idea of “yoke” is what Jessamyn Stanley calls the yoga of the everyday — a yoga that is not just about perfecting your downward dog but about applying the hard lessons learned on the mat to the even harder daily project of living.”

Just As I Am (Cicely Tyson & Michelle Burford)

This memoir by the late, great actress and advocate, Cicely Tyson, likely needs no introduction, but it’s here because it needs to be on reading list of everyone-who-hasn’t-yet-read-it this summer.

From the words of Ms. Tyson herself, “Just as I Am is my truth. It is me, plain and unvarnished, with the glitter and garland set aside. In these pages, I am indeed Cicely, the actress who has been blessed to grace the stage and screen for six decades. Yet I am also the church girl who once rarely spoke a word. I am the teenager who sought solace in the verses of the old hymn for which this book is named. I am a daughter and a mother, a sister and a friend. I am an observer of human nature and the dreamer of audacious dreams. I am a woman who has hurt as immeasurably as I have loved, a child of God divinely guided by his hand. And here in my ninth decade, I am a woman who, at long last, has something meaningful to say.”

Once Upon A Time, Enslaved Africans Were An Insurance Commodity

Slave insurance was one of America’s earliest forms of industrial risk management that provided an important source of revenue for companies

By Dr. Stacey Patton

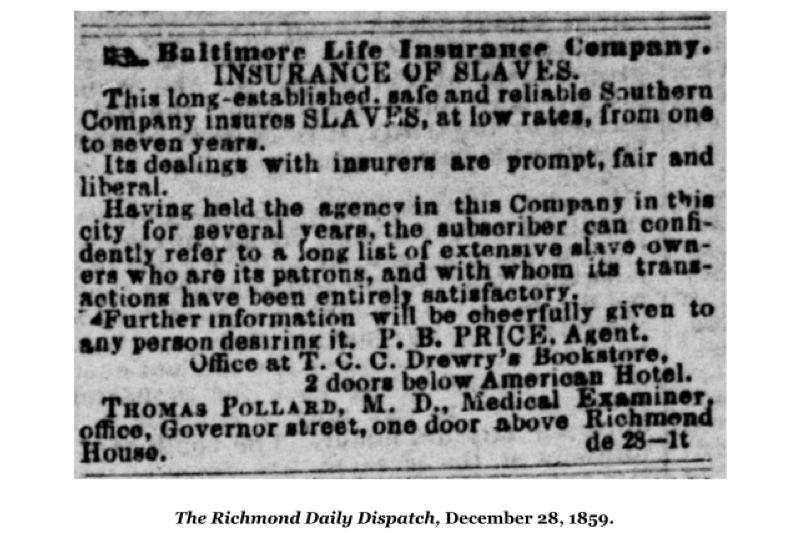

On the morning of April 20, 1859, a terrible explosion rocked the Bright Hope Coal Pits in Chesterfield County, Virginia, about 18 miles from the Richmond Railroad.

The tragedy claimed the lives of nine men, four of whom were white. Their names were solemnly printed in local newspapers across the South: Isaac Farmer, George Smith, Nicholas Blankenship, and Albert Rowe.

A dispatch from the Kanawha Valley Star reported: “The explosion created great excitement, and every effort was made to descend the shaft and to rescue the unfortunate men, dead or alive, but it was impossible to do so, because of the life destroying gasses, which seemed to fill the entire shaft.” The bodies were believed to have been entirely consumed in the explosion.

Among the victims were also five Black males whose names did not make it to the public record.

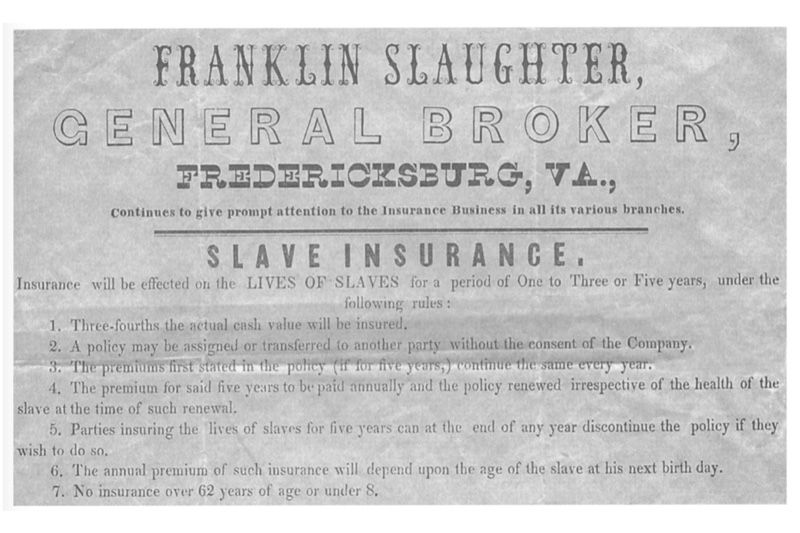

Press accounts identified those Black victims as “servants.” But they were slaves owned by four different white masters, male and female, and their deaths were noted only in terms of property loss. Archival records reveal that all five slaves had an insurance policy taken out on them, valued at $800 each, roughly equivalent to around $29,000 in today’s dollars. Payouts from the insurance policies likely went entirely to the purchaser of the plans, the slaveholders, leaving the loved ones of those victims still enslaved and penniless.

This incident sheds light on a grim chapter in American history, during which human lives were commodified and insured as property by some of the largest insurance companies in the world.

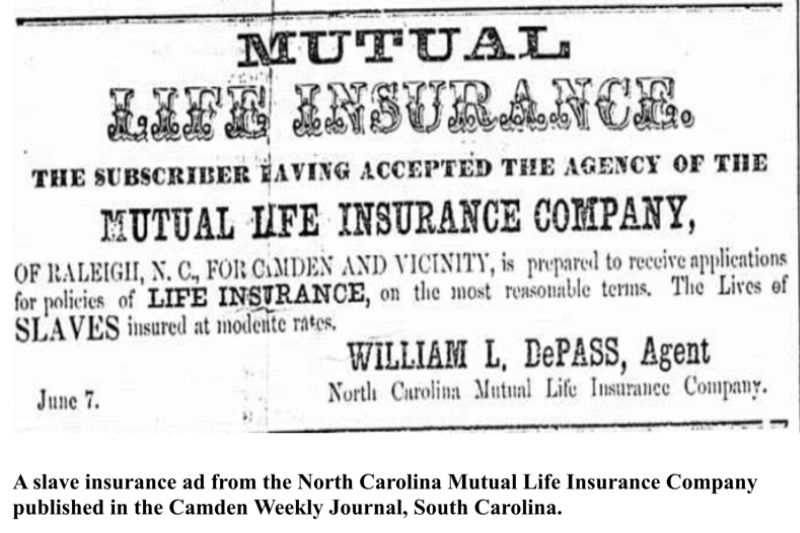

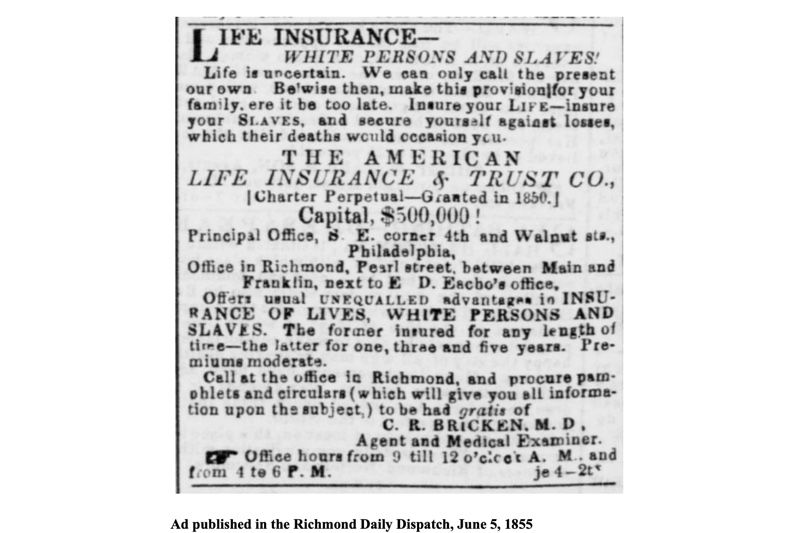

Several historians have noted that slave insurance was one of America’s earliest forms of industrial risk management that provided an important source of revenue for companies that included Baltimore Life, New York Life, AIG, Aetna, American Life, Virginia Life, Richmond Fire Association, North Carolina Mutual Life Insurance Company, Asheville Mutual Insurance Company, Lynchburg Hose and Fire Insurance Company, Greensborough Mutual Life, and others. It is important to note that Aetna Life first issued policies in 1853 out of Hartford, Connecticut, even though slavery had been illegal in the state since 1848.

Slave policies were not just about mitigating financial loss for white owners; they reveal a systemic dehumanization where the value of a human being was reduced to a mere monetary figure. Understanding the history of insurance companies and their role in perpetuating slavery can help us see the pervasive nature of racial dehumanization and its deep-seated roots in America’s financial systems.

Two years before the Bright Hope explosion, in February 1857, the hiring agency Tompkins & Company insured 14 slaves – ages 12 through 50 – to work in the nearby Black Health Coal Pits for one year. In January 1855, Richmond merchant Joseph Winston insured his slave Andrew, age 11, for $400 to work in a cotton factory across the river in Manchester. The policy term was for seven years, but Andrew died before the policy expired. Flash back even further to September 1843. Daniel Zacharias of Frederick, Maryland, insured his 27-year-old slave Robert Randall, a brickmaker, for $200. He, too, died near the end of the seven-year policy.

The coincidence of both an enslaved boy and a man dying before the expiration of their insurance policies raises troubling questions about the conditions they endured and the broader implications of insuring enslaved people. Their premature deaths, along with the Bright Hope victims, suggest a common thread of harsh and hazardous conditions that enslaved people faced daily. The backbreaking labor, whether in a cotton factory, coal pit, or as a brickmaker, the lack of medical care, and the overall brutal treatment inherent in slavery likely contributed to shortened lives.

While the exact circumstances of the 11-year-old boy and 27-year-old man remain unknown, this pattern of premature death invites speculation that the very act of insuring these Black lives might have inadvertently incentivized their owners to push them beyond their limits, knowing there was financial compensation in case of their demise. For enslaved men who would otherwise be considered unskilled, by the time they were in their mid to late 20s, were valued anywhere from $700 to $1,000 on average, according to appraisal values. This sum would be comparable to contemporary funds needed to purchase a starter car or put a down payment on a basic home, a range from $23,000 to $36,000.

The deaths of those Virginia and Maryland victims were more than just footnotes in history; they underscore the intersection between human suffering and financial exploitation. Enslaved people were considered liquid capital, able to be traded, sold, and rented as their enslavers saw fit.

Not only could they generate income through their labor, but their existence caused them to appreciate in their value until their mid-30s. Enslaved individuals considered skilled, whether as craftsmen, boatmen, or sawmill workers, could be valued at up to three times the price of the average field hand. This increase was due to the time and funds spent training individuals to be proficient in their assigned skills. Because of the high appraisal value, owners had more incentive to protect their human investment, leading to their utilization of insurance policies.

Historians tell us that life insurance did not become popular in the U.S. until the late antebellum period, from the 1830s until the start of the Civil War. People rarely had their lives insured and did not buy policies to cover the everyday risks on their lives or to protect the surviving spouses and children in case of the loss of the main breadwinner.

According to Todd Savitt, a leading scholar on slave life insurance, the first companies to offer the sale of life insurance policies included the Insurance Company of North America (1794), the Pennsylvania Company (1809), Massachusetts Hospital Insurance Company (1818), the New York Insurance Trust Company (1830), and Girard Life Insurance and Trust Company (1836). More than a dozen insurance companies were founded in the southern and border states between 1840 and 1860.

Prior to the mid-19th century, insurance companies had issued policies mostly confined to merchants who were transporting their captive human cargo. Due to the treacherous nature of the Middle Passage journey, there was a high chance for the loss of life, which translated into a loss of profit for slave ship owners. Once the trans-Atlantic slave trade was made illegal through an act of Congress in 1808, insurance companies turned their focus to enslaved populations already in the U.S. as appraisal values of Black lives began to rise.

Savitt notes that whites were increasingly insuring the lives of their slaves, but not in overwhelming numbers due to high costs. Though agents frequently advertised in local papers, owners were reluctant to shell out an extra $5 to $15 annually for each slave. Not to mention, there was confusion among owners between slaves as people and slaves as property. Horses, barns, and crops were often insured. So, what did this mean for an enslaved individual? When owners hired out a slave or rented one for a dangerous industrial job, the slave was obviously a piece of property, and the investment required financial protection.

According to Sharon Ann Murphy’s article, “Securing Human Property: Slavery, Life Insurance, and Industrialization in the Upper South,” the development of insurance policies for enslaved people emerged and grew significantly in the decades leading up to the Civil War. She explains that between the American Revolution and the Civil War, slavery in the U.S. underwent dramatic change. Initially concentrated in the production of tobacco, rice, and indigo along the southeastern coasts of Virginia and the Carolinas, slavery began to shift geographically and economically, with the rise of cotton as a dominant staple.

The invention of the cotton gin in 1793 and increasing demand from the British textile industry made large-scale cotton production highly profitable. This economic boom led to new settlements in the Lower South states, including South Carolina, Georgia, Alabama, Mississippi, Louisiana, and eastern Texas. As cotton prices surged, so did the demand for enslaved labor, driving up the prices of enslaved people.

Faced with declining tobacco profits and increasing labor costs, Upper South slaveholders sought new ways to profit from their enslaved populations. In the 1840s, with new industries opening en masse – steamboat operations, public works construction, iron manufacturing, railroads, coal mines, and cotton mills – enslaved people’s labor was redirected to these dangerous ventures. According to Murphy’s research, slaveholders also engaged in a vibrant internal slave trade, which saw over 700,000 slaves sold to the Lower South between 1790 and 1860. Owners rented or leased their slaves’ labor to companies and collected the income without having to supply food, housing, and clothing. Rental policies were often year-to-year, and so too were insurance policies. Murphy notes that these economic shifts paralleled the emergence of a life insurance industry in the northeastern U.S., which also saw an opportunity to insure enslaved people as property.

At inception, life insurance was mainly a northern-based industry. While Savitt’s research found that only about three percent of all industrial slaves and a substantially smaller number of plantation slaves in any year in the 1850s were covered by insurance, Murphy contends that by the eve of the Civil War, demand for slave insurance grew rapidly in the South. This demand paralleled the growth in policies on northeastern whites, and slaveholders were at the forefront of those who embraced this new product.

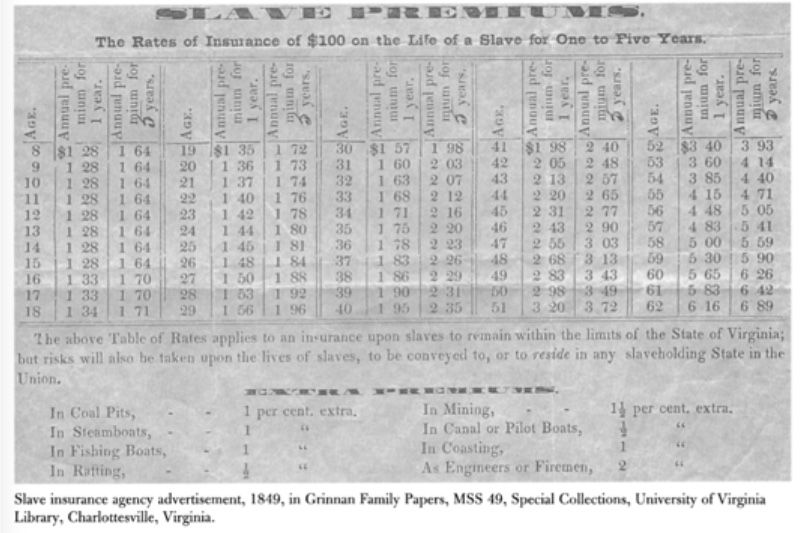

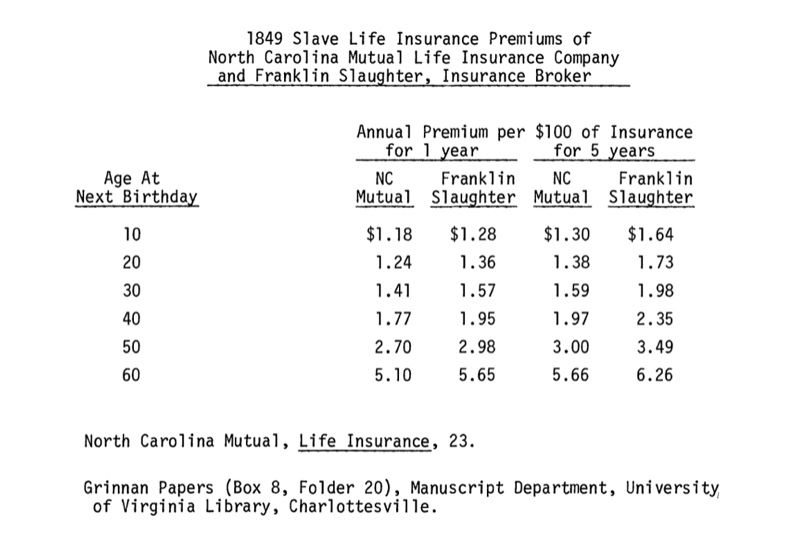

Companies limited the amount for which a slave could be insured, as well as the length of policy terms – four to five years for slaves ages 10 to 60 years old, while whites could purchase policies for life at a set annual premium. Slaves were not insured for their full value. To protect themselves from paying out more than necessary, companies refused to issue policies worth more than $800 or two-thirds or three-quarters of the appraised value of an enslaved person. The North Carolina Mutual Company included a stipulation that said, “in case the said slave shall die for want of proper medical or personal attendance … this Policy shall be void.”

Insurance companies also prohibited the free movement of insured slaves from region to region and charged extra premiums for dangerous jobs while requiring reputable medical doctors to examine individuals prior to policy approvals. Those doctors also received fees for their services, ranging from 15 cents to two dollars per exam. Enslaved individuals could be denied coverage for having chronic diseases, being of unsound mind, or for pregnancy.

If we examine insurance premium tables from the era, it is evident that starting at about age 32 for whites, premiums increased by five cents per plan year-to-year. By the 40s, the premiums were for a full dollar more than those for insuring an enslaved person even a decade younger. Most insurance companies preferred to insure enslaved people in the prime of their health, typically during late adolescence to young adulthood. Slaveholders, when considering the extra expense of purchasing insurance, would most likely insure men over women. Women were not only susceptible to higher mortality rates due to childbirth, but many enslavers also viewed them as more easily replaceable because their value was often tied to their reproductive capacity, as Daina Ramey Berry’s book The Price for their Pound of Flesh shows.

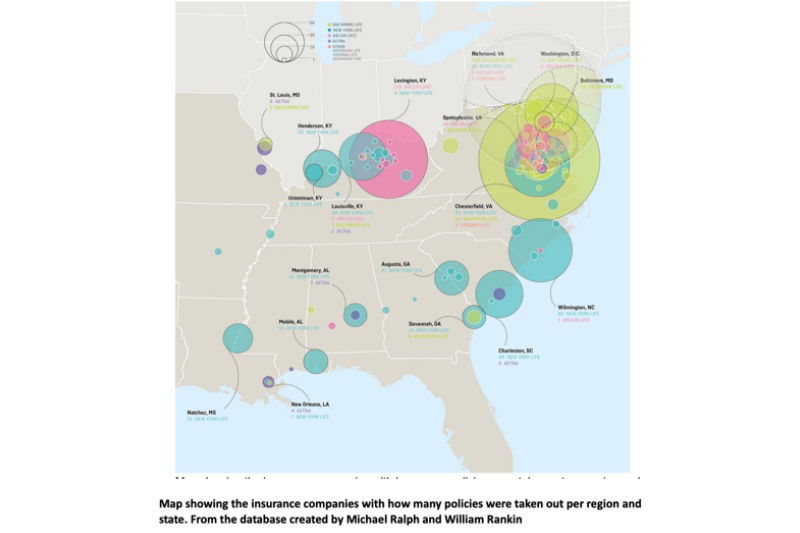

Due to the high expense of insurance policies, the average slaveholder could not afford to insure their bondsmen. Typically, there would be either one enslaved person under a policy for one owner or roughly ten policies under one owner. A.P. Scott of Fayette, Kentucky, had 18 policies on enslaved men at some point in the 1850s. His neighbors had their enslaved people insured for jobs such as firemen and boat navigators. Most insured were men, with their policies listed in Alabama, Arkansas, the District of Columbia, Georgia, Kentucky, Missouri, Mississippi, the Carolinas, and Virginia.

Despite the large number of enslaved people held hostage in the United States, comparatively few insurance policies were taken out on them. Over roughly two decades, from the 1840s to the early 1860s, only about 1,000 policies were issued by larger, cross-state companies. While smaller companies, many of which have since gone defunct, issued more policies than have been formally recorded, even assuming those companies together comprised another 1,000 policies, this would still represent a fraction of a percent of all the enslaved people who existed during that time. In 1860 alone, there were almost 4 million enslaved people in the United States. At any one point in time, there would likely have been only a few hundred policies on enslaved people per year.Several million dollars were historically stored in life insurance policies. Policies on enslaved laborers tended to have higher premiums, as many companies went bankrupt due to heavy losses and insurance claims related to deaths from disease.

The Civil War and Emancipation had a profound impact on insurance companies that had issued policies on enslaved people.

With the abolition of slavery following the Civil War, the property that these policies insured – enslaved individuals – no longer existed in legal terms. This effectively rendered all such policies null and void, as the insured “property” had been emancipated.Insurance companies that had issued these policies faced significant financial losses. Many policies were long-term, and the companies had collected premiums with the expectation of providing coverage over the entire term.

The sudden end to slavery meant that these companies could no longer collect premiums or fulfill their obligations under the policies, leading to potential disputes and financial instability.The end of slavery forced insurance companies to reassess their business models and reputations.This likely involved diversifying their policy offerings and focusing on other areas of life and property insurance.

What if slavery had continued beyond the Civil War?

Insurance companies would likely have seen an expansion in the market for slave policies. As the institution of slavery grew or remained stable, more slaveholders might have sought to insure their enslaved people to protect their investments, leading to a larger, more lucrative market for these insurance products.With continued demand for slave insurance, companies might have developed more specialized and varied insurance products tailored to different types of enslaved labor, such as field hands, skilled laborers, and domestic servants. Innovations could have included policies covering not only death but also injury, escape, and loss of productivity.

In the aftermath of slavery, insurance companies charged Black people higher rates for life insurance than whites. Their premiums were based on racist theories about Black bodies, health, longevity, and social habits. Meanwhile, Black mutual aid societies, which had been established during the antebellum period, continued to support Black communities as an early form of insurance to ensure proper burials and support for surviving loved ones.

Scholars have noted that at least 1,300 antebellum-era policies have been found in the archives of the world’s largest insurance companies, and evidence suggests that at least 85% of policy records have been lost. So, what does this mean for our understanding of the full scope of insurance companies’ involvement in perpetuating slavery?

This significant loss of records means that the full extent of insurance companies’ involvement in slavery is likely much greater than what current evidence shows. The surviving records are only a fraction of the total number of policies that were likely issued. This incomplete historical record suggests that many more enslaved individuals were insured, and insurance companies played a more extensive role in the economic mechanisms that sustained and profited from slavery.

Since 2004, several states have required the disclosure of their ties to slavery, producing documents from their archives and former records. Beyond being tasked with making their archives and records public, there does not appear to have been much further action taken to provide reparations to those whose ancestors were formerly enslaved.

Tiana’s Bayou Adventure Brings Black Magic To Magic Kingdom

During the month of Juneteenth, Disney World has unveiled Tiana’s Bayou Adventure

During the month of Juneteenth, Disney World will unveil Tiana’s Bayou Adventure, one of its Blackest attractions yet—and it is nothing short of magical much like the Black talent involved with the concept.

The amusement park company invited media to the exclusive preview and a star-studded shindig that highlighted New Orleans culture and integral collaborators who brought the adventure to fruition. In attendance was Stella Chase, daughter of Leah Chase, award-winning chef of Dooky Chase restaurant in New Orleans, along with grandson Edgar “Dook” Chase and granddaughter Myla Reese Poree; jazz musicians Terence Blanchard and PJ Morton; talk show host Tamron Hall; Anika Noni Rose, the voice of Princess Tiana in the Disney animated film Princess and The Frog; and Mama Odie herself, Jenifer Lewis, to name a few.

“I’m excited. It’s us. It’s special because I’m so many ways we built this country and we should be represented everywhere…but here we are.” The Black-ish actress said. “This will be here forever.”

At the helm of it all was Sivonne Davis, vice president of marketing strategy for Walt Disney World Resort. Davis spoke to the intentionality around inclusion and representation and to the commitment and passion it took to accomplish such a feat.

“It is my critical responsibility to showup for others, to everyone, quite frankly.” Davis told BLACK ENTERPRISE.

“I try to make sure I have a connection with everyone, especially making sure people like myself feel like they see themselves and see the possibilities,” she said. “Sherita said it brilliantly, ‘It has been a love story to Louisiana,’ but it’s also a love story to our cast and to Walt Disney World bringing forth all the possibilities in a brilliant way.”

Blanchard was ecstatic about experiencing the Disney moment with his children and grandchildren and bringing an authentic New Orleans sound to the production.

“Baby, let me tell you something,” the famed musician told BE. “Disney is about family … I have my son and my grandson here with me and we’re just hanging out and having a great time. What can beat that?”

Blanchard added, “I did the music for the Q-line, and it’s all New Orleans-based music with New Orleans musicians and brass bands. Leah Chase is singing. I’m performing. Hopefully, you all can get a sense of the history of the music from the city and hopefully it can spark some interest.”

Tiana’s Bayou Adventure

It starts with a walkthrough of Princess Tiana’s Palace, where park-goers are surrounded with family history that is inspired by Leah Chase, the famous New Orleans restaurateur and her family legacy. Notable features are the portraiture that line the walls, memorabilia which fills the rooms, jazz as the backdrop, and the smell of beignets in the air. After traveling through nostalgic times, a log boat awaits riders.

Thrill seekers are in for a treat as a colossal-sized princess Tiana introduces the adventure and offers a word of caution to riders before entering at their own risk.

Riders then float all up and through a lagoon designed to mimic a New Orleans swamp ride, experiencing all the twists and turns and splashing water that comes with each curve up until the final 52.5 foot drop. The color array of animatronic characters and scenes throughout the adventure will excite children and adults.

Tiana’s Bayou Adventure officially opens at Disney’s Magical Kingdom on Thursday, June 28.

Resident Poet Jasmine Mans To Showcase Poetry In 2-Night Performance

Mans is the first resident poet at Express Newark and her work is deeply influenced by her upbringing in Newark's South Ward.

Jasmine Mans, the inaugural resident poet at Express Newark, has garnered both critical acclaim and commercial success with her 2021 poetry collection, Black Girl, Call Home.

On June 27 and 28, Mans will showcase her artistry in a two-night poetry performance at Express Newark, supported by New Arts Justice, a public arts initiative founded by Pulitzer Prize-winning Rutgers-Newark Professor Salamishah Tillet in 2018.

Many poems in Black Girl, Call Home focus on Mans’ mother, exploring adolescent conflicts and the complexities of their relationship. Her work is deeply influenced by her upbringing in Newark’s South Ward, where her great-grandparents settled in the 1920s after migrating from Georgia.

“As a Black woman, you’re taught to think there’s something wrong with yourself, and if you’re from the so-called hood, to think there’s something wrong with where you grew up,’’ Mans said. “But even though I don’t come from a place of financial wealth, I inherited a sense of music, style, and food. My family is thick in love and culture.’’

In homage to Newark’s literary giant LeRoi Jones, later known as Amiri Baraka, Mans crafted a poetic tribute inspired by his seminal 1963 work, “Blues People.” This piece served as a cornerstone for the exhibition’s debut. Building on this foundation, Mans has embarked on a creative journey with Express Newark, producing a series of bi-weekly video releases showcasing her latest compositions. Her upcoming performances at Express Newark promise to be a rich exploration, delving deeper into the cultural tapestry woven by “Blues People.”

As artist-in-residence, Mans has created “Daughter,” a piece exploring voice, memory, and reclamation, accompanied by a live band. “It’s a big deal to be the only poet in this space…writing to build out a show and a portfolio of poetry that represents not only ‘Blues People,’ but the people of Newark,” she said.

Mans is preparing her next poetry collection for 2026. Additionally, she’s editing a coffee table book titled Buy Weed From Women, slated for publication by Penguin Random House in 2026. This project celebrates women’s roles in the cannabis industry, from farmers and entrepreneurs to those navigating the intersection of profit and criminality.

Diddy Drops Sean John Lawsuit As Other Legal Battles Continue

Diddy and Global Brands Group agreed to the voluntary dismissal of the claims and counter-claims on June 21.

Sean “Diddy” Combs has dropped his lawsuit against self-founded Sean John for using his name, as his other legal battle continues. Diddy originally founded the clothing brand in 1998.

Diddy’s lawsuit was against Global Brands Group (GBG), to which he sold his 90% stake in Sean John for $70 million in 2016. However, the media mogul accused the company of using his name and persona to boost sales. He has filed multiple lawsuits since February 2021, per AllHipHop.com.

Diddy won back the company in a $7.5 million bid in 2021 but his quest for a payout from the now-bankrupt GBG continued. In one instance, Diddy claimed that the GBG-owned Sean John’s collaboration with fellow clothing brand Missguided used his image as a promotion without his consent.

The two parties agreed to the voluntary dismissal of the claims and counterclaims on June 21. In the legal filing, he originally sought $60 million. However, lawsuits against him have forced Combs to drop the case.

This slew of lawsuits began with the November 2023 lawsuit filed by his ex-partner, Cassie Ventura. Ventura agreed to a settlement the day after filing, which led to other women coming forward with accusations against Combs.

Moreover, a 2016 video released to the public in May proved Ventura’s allegations against him. The clip further disgraced the entertainer, who has recently shied away from the limelight. Other lawsuits, including claims of sexual harassment and sex trafficking by his former producer, remain ongoing.

Diddy has also stepped down from his role at Revolt, while other entities have distanced themselves from the now-infamous producer. Most recently, Howard University revoked his honorary degree, and New York City also rescinded his key to the city.

While currently dealing with numerous lawsuits, Diddy can sue GBG again for the same claims in the future.